- AlphaInsights by 8alpha.ai

- Posts

- War’s Cost: Your Wallet

War’s Cost: Your Wallet

Nicole Rojas

March 23, 2026

Week of March 23rd, 2026

Welcome to AlphaInsights, 8alpha.ai’s weekly newsletter, your ultimate source for curated insights and key updates from the dynamic world of venture capital!

From billion-dollar rounds to market-defining shifts, we deliver the intelligence powering the global investment landscape, moving investors and innovators forward. At 8alpha.ai, we’re not waiting for the future of capital, we’re building it. Stay sharp, stay curious, and stay ahead.

STARTUPS

ROUNDS AND UNICORNS

The Week’s 10 Biggest Funding Rounds: Investment Slows, But Security And AI Remain Top Picks (Crunchbase, 5 minute read)

Cloaked ($375M, privacy): Led by General Catalyst and Liberty City Ventures, the Massachusetts-based consumer privacy platform raised $375M in Series B funding

Frore Systems ($143M, AI infrastructure): At a $1.64B valuation, the San Jose–based AI cooling hardware company closed a $143M Series D round led by MVP Ventures

XBow ($120M, cybersecurity): Valued at over $1B, the Seattle-based autonomous security testing startup raised $120M in Series C funding from DFJ Growth and Northzone

Oasis Security ($120M, cybersecurity): Backed by Craft Ventures, Cyberstarts, Sequoia, and Accel, the identity security startup raised $120M, bringing total funding to $195M

Imperative Care ($100M, medical devices): The Campbell, California–based medical device company secured $100M in convertible financing led by Elevage Medical Technologies and Perceptive Advisors

The Rising Investors Behind The New Unicorn Class (Crunchbase, 5 minute read)

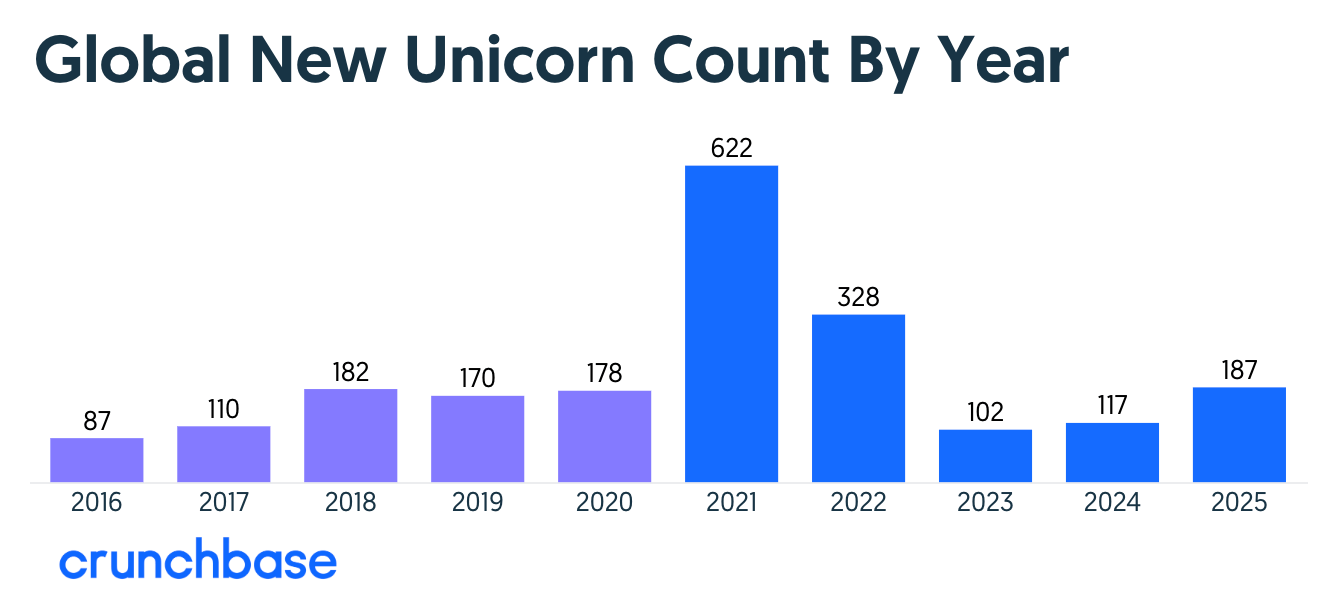

Unicorn creation surged in 2025, with 187 new billion-dollar startups (+61% YoY), marking a strong rebound above post-pandemic levels and slightly ahead of pre-2020 norms. Growth was fueled by AI, which produced 47 new unicorns (25%), a share expected to rise further. Notably, 94 companies (~50%) reached unicorn status in under 5 years, signaling faster scaling cycles

Examples of this new cohort include OpenEvidence (medical AI), Kalshi (prediction markets), Reflection AI (frontier AI lab), Hippocratic AI (health support), and Decagon (AI customer support)

Overall, the unicorn landscape is expanding rapidly, with higher valuations, shorter timelines, and increasing concentration around AI-driven companies

Opportunities and risks of White House’s proposed AI policy (PitchBook, 5 minute read)

The White House’s proposed AI regulatory framework signals a pro-industry approach that favors startups and investors, including efforts to limit state-level AI regulation, after 3+ years of stalled federal efforts, expand tax incentives and grants, and increase access to federal datasets for AI training. It also supports streamlined permitting for AI infrastructure and stronger action against AI-driven scams, benefiting cybersecurity startups

However, it shifts more energy infrastructure costs onto data center operators, even as firms like Blackstone have already invested $1.2B in related energy projects

While not yet law, the framework outlines federal priorities but faces uncertainty due to competing proposals and political gridlock ahead of upcoming elections

ECONOMIC SNAPSHOT

Federal Reserve chief Jay Powell says Iran oil crisis will worsen US inflation (Financial Times, 5 minute read)

Fed Chair Jay Powell warned that the Iran war is fueling a surge in energy prices, with oil reaching ~$99/barrel (up ~50%), which is expected to push inflation to ~2.7% (vs. 2.4% prior), still above the Fed’s 2% target. The Fed held rates steady at 3.5%–3.75% for a second meeting, as it balances rising inflation risks with a weakening economy, including 92,000 job losses and a sharp slowdown in growth to 0.7% (from 4.4%)

Markets have turned more cautious: 2-year Treasury yields climbed to 3.77% (highest since Aug 2025) and the S&P 500 fell 1.4%

Expectations for rate cuts have also shifted out to 2027, compared to earlier expectations of multiple cuts

Despite projections for at least one rate cut in 2026 (12 of 19 officials), uncertainty remains, with some policymakers even considering hikes

Iran War poses ‘major, major threat’ to global economy, energy chief says (Fortune, 6 minute read)

The U.S. government’s fiscal position continued to weaken in 2025, with $6.06T in assets versus $47.78T in liabilities, resulting in a -$41.7T deficit position (a ~$2.1T decline YoY), largely driven by rising federal debt ($30.3T) and obligations for federal employees and veterans ($15.5T). Beyond the balance sheet, long-term commitments for Social Security and Medicare reached $88.4T over 75 years (+$10.1T YoY), bringing total projected obligations to roughly $136T (~5× U.S. GDP). While these figures may appear alarming, much of this reflects long-term demographic and healthcare cost trends rather than near-term cash needs

The data highlights a growing structural imbalance between revenues and future spending commitments

This underscores the importance of policy decisions around taxation, entitlement reform, and economic growth

Persistent accounting issues, including 29 consecutive audit disclaimers, limit visibility into the government’s full financial position, highlighting the need for greater transparency

What $4-a-gallon gasoline means for you and the economy (CNN, 5 minute read)

U.S. gas prices are approaching $4 per gallon for the first time since 2022, driven by a ~$30 surge in oil prices, which has already lifted pump prices by roughly $0.90. This energy shock is expected to reduce GDP growth by ~0.3pp, increase inflation from ~2.4% to potentially 3.5%–4%, and raise household costs by about $450 annually for every $10 increase in oil

While the U.S. economy remains resilient, rising fuel costs are beginning to shift consumer behavior, with some households cutting travel and discretionary spending

If prices climb above $4.25 per gallon and oil exceeds $125, demand could weaken more sharply

With a cooling labor market and high living costs, rising energy prices are adding pressure and prolonging inflation

US regulators slash Wall Street capital rules to boost bank lending (Financial Times, 5 minute read)

U.S. regulators are proposing a significant easing of bank capital rules, cutting requirements by ~4.8% for the largest banks (>$700B in assets), 5.2% for midsized banks, and up to 7.8% for smaller lenders, reversing earlier proposals that would have increased requirements by ~19%. The reforms, tied to Basel III updates, stress test changes, and lower capital charges on assets like mortgages, could free up roughly $117B in capital from a ~$2T base, potentially boosting lending, share buybacks, and M&A activity

The move reflects a broader policy shift nearly two decades after the 2008 crisis, aimed at improving bank competitiveness

However, critics warn it could weaken the financial system resilience

IPOs & EXITS

Small And Mid-Sized Startup Purchases Are Still Well Below The 2021 Peak (Crunchbase, 4 minute read)

Startup exits tend to fall between blockbuster wins and distressed sales, with a large share occurring in the “in-between” category of sub-$300 million acquisitions. While these deals generate less attention, they collectively totaled about $8.7 billion in the U.S. last year, though still below levels seen a decade ago. Their impact is also dwarfed by mega-deals, such as Google’s $32 billion acquisition of Wiz, which alone exceeds 4× the value of all sub-$300M exits combined

Activity is recovering post-2023–2024 lows, but smaller deals remain weak

Returns are mixed, with both profitable and below-cost exits

The market is fragmented: across 181 sub-$300M deals since 2024, no buyer did more than two, and many prices are undisclosed

The Most Active Startup Acquirers Of The Past 3 Years Aren’t Always Who You’d Expect (Crunchbase, 3 minute read)

Startup acquirers vary widely, from big tech and pharma giants to fast-growing unicorns and newer public companies, but a small group stands out for high-volume dealmaking. Over the past three years, 79 companies made at least three acquisitions, with Salesforce, OpenAI, and Snowflake among the most active; notably, OpenAI completed 16 deals and Snowflake 19 in that period

However, the most active buyers are not always the biggest spenders, as Google’s $32B acquisition of Wiz far exceeds others

M&A activity remains strong into 2026, with large deals like Capital One–Brex ($5.15B) and Eli Lilly–Orna ($2.4B), alongside continued momentum from smaller AI-driven acquisitions

PwC’s US IPO Lead On The 2026 Outlook, IPO Timing And The Secondary Boom (Crunchbase, 6 minute read)

The tech IPO market has been slow to start in 2026, but a strong pipeline, including potential listings from SpaceX, OpenAI, and Anthropic, could reignite activity. Delays are driven by a mix of macro uncertainty, a backlog of 900+ SEC filings from the 2025 shutdown, and a shift toward “readiness over timing,” with companies now preparing 18–24 months in advance before going public. Despite the slowdown, fundamentals remain strong, with 800+ IPO-ready unicorns waiting in the pipeline

Investor expectations have also reset: markets now favor scaled, cash-generative companies with clear paths to profitability, rather than growth at any cost

At the same time, secondary markets (>$60B in 2025) are allowing founders to delay IPOs, pushing the median time to IPO to 11+ years

Despite this, IPOs remain the “gold standard” for liquidity and long-term positioning

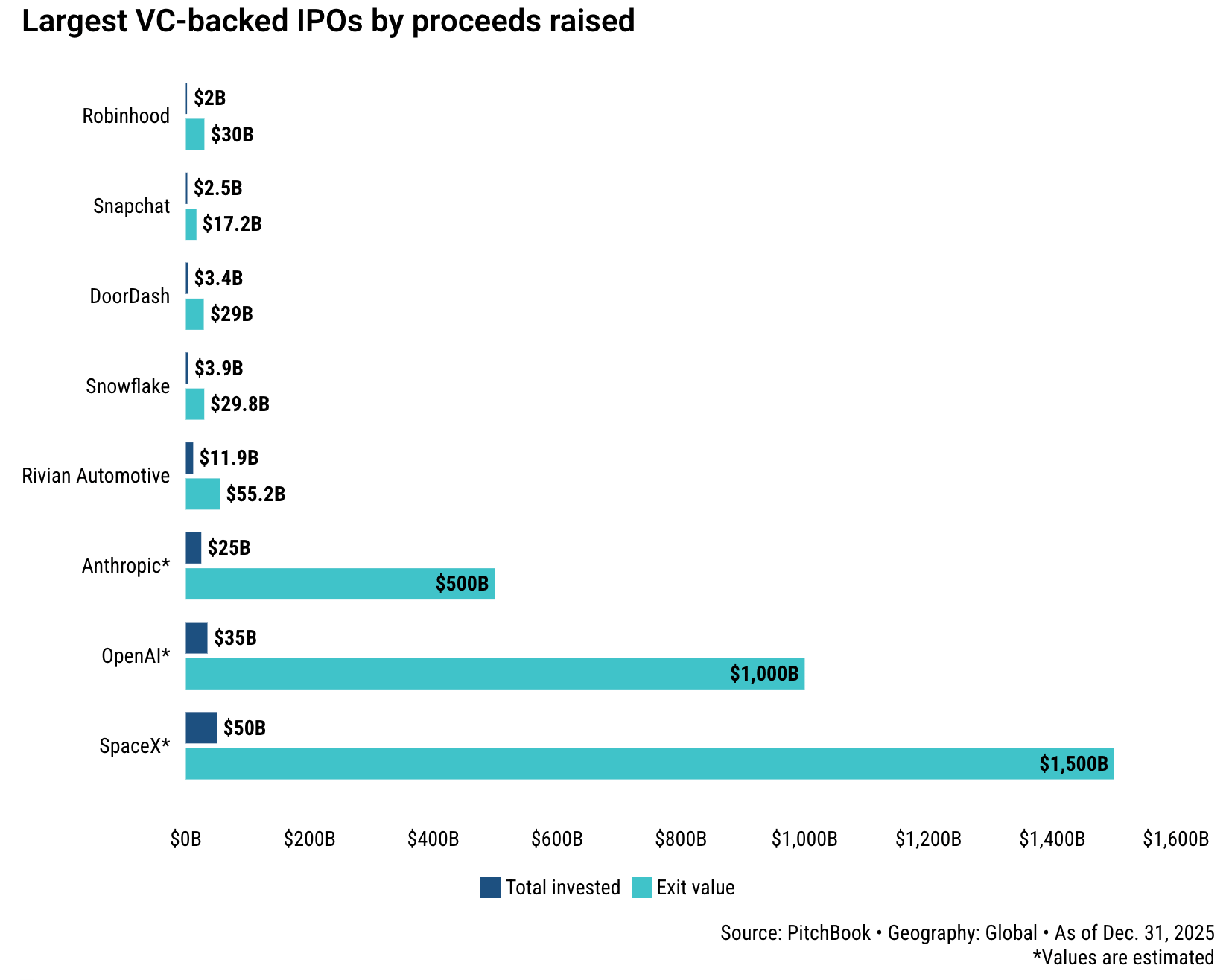

The mega IPOs that could shut out the rest of VC (PitchBook, 3 minute read)

The 2026 IPO market, expected to rebound, may instead be dominated by three mega-listings, SpaceX ($1.25T), OpenAI ($840B), and Anthropic ($330B), which together could raise $100B+ and represent a combined ~$2.4T valuation, exceeding the total value of all U.S. VC-backed IPOs since 2000. While this would be a major win for venture capital, it could concentrate liquidity among a few players, strain underwriters, and absorb public market capital, crowding out other unicorns

With few companies currently in registration, no major IPOs early in 2026, and a 4-year liquidity drought, the market remains fragile

These mega-IPOs could either reopen the market or delay recovery further if post-IPO performance disappoints

WHAT A TIME TO BE ALIVE

‘They’ve Stolen the Narrative’: Black Business Leaders on the DEI Backlash (Bloomberg, 5 minute read)

Black leaders in the U.S. are navigating a challenging environment as political pushback against DEI intensifies, with the Trump administration targeting initiatives and influencing corporate behavior. Despite this, executives emphasize that diversity is not just ideological but performance-driven, with 87% of diverse teams making better decisions, while also noting increased Black representation across sectors (e.g., more Black senators, legislators, and fund managers than ever)

However, many report reduced opportunities, fewer leadership calls, and growing caution among professionals

The discussion highlights a recurring pattern of progress followed by backlash, while stressing the importance of maintaining visibility, mentorship, and long-term efforts to sustain inclusion and economic advancement

FEMA to Relaunch Climate Resiliency Grants, Complying With Court Order (The New York Times, 5 minute read)

The Federal Emergency Management Agency (FEMA), the U.S. agency responsible for disaster response and preparedness, is reinstating its Building Resilient Infrastructure and Communities (BRIC) grant program after a federal judge ruled its cancellation illegal in a lawsuit brought by 22 states. The program, designed to fund preventive infrastructure against disasters like floods, wildfires, and hurricanes, had already deployed ~$4.5B and helped avert an estimated $150B in damages over two decades

Its revival underscores a shift back toward proactive disaster mitigation, even as debates continue over federal spending priorities and the role of climate-focused programs

AI8 VENTURES HIGHLIGHT

State of VC Report: The AI Power Law

“Every technological revolution has two halves: the bubble and the golden age that follows.”

The stock market is at all-time highs, but inflation remains sticky and the job market is weakening. Ask around and you’ll hear the same refrain: the labor market feels tougher than ever. At the same time, the first wave of AI agents is “joining the workforce”. Imagine a software engineering agent capable of performing most tasks of a mid-level developer. Now imagine thousands. Extend that across every knowledge field, and the implications for productivity, and potential displacement, are profound.

What happens when the next round of layoffs hits? Add tariffs on top, and ask what happens if consumption weakens. Even the Federal Reserve admits it is unsure of what comes next.

Against this backdrop, venture capital in 2025 is not in recovery but in recalibration. The illusion of recovery is powered almost entirely by AI. Capital is flowing, but to fewer companies than ever. Outside AI, down rounds are rising, and nearly half the unicorn population hasn’t raised since 2022.

We are living in an AI bubble. Just four mega caps, Nvidia, Meta, Microsoft, and Broadcom, accounted for 60% of the S&P 500’s gains, with Nvidia alone responsible for more than a quarter. It’s a paradox. Yes, we’re in a bubble, but it’s also the future. We are witnessing what may be the most important technological shift in a generation. It’s hype layered on top of something undeniably real.

Uncertainty is the name of the game; not one single path forward, but divergent scenarios. Alpha will be earned through selectivity, by navigating volatility rather than avoiding it.

8alpha.ai is an AI fintech transforming cash-generating businesses into scalable, AI-powered companies. We provide revenue-based financing and hands-on AI transformation, delivering no zeros with unlimited upside. We’re the architects building financial infrastructure for the next generation of investors and startups.

Become part of our revolution.

Happy reading,

8alpha.ai’s Research & Investment Team