- AlphaInsights by 8alpha.ai

- Posts

- Tariffs Never Left.

Tariffs Never Left.

Nicole Rojas

February 23, 2026

Week of February 23rd, 2026

Welcome to AlphaInsights, 8alpha.ai’s weekly newsletter, your ultimate source for curated insights and key updates from the dynamic world of venture capital!

From billion-dollar rounds to market-defining shifts, we deliver the intelligence powering the global investment landscape, moving investors and innovators forward. At 8alpha.ai, we’re not waiting for the future of capital, we’re building it. Stay sharp, stay curious, and stay ahead.

STARTUPS

ROUNDS AND UNICORNS

The Week’s Biggest Funding Rounds: World Labs Leads Another AI-Heavy Lineup (Crunchbase, 5 minute read)

World Labs ($1B, spatial AI): The San Francisco startup founded by Fei-Fei Li raised $1 billion to build foundational 3D world AI models, with backing from investors including Nvidia, AMD and Fidelity

Vestwell ($385M, fintech): The New York-based savings platform secured $385 million in Series E funding at a $2 billion valuation, led by Blue Owl Capital and Sixth Street Growth

Temporal Technologies ($300M, workflow software): The Bellevue company raised $300 million in Series D funding led by Andreessen Horowitz, reaching a $5 billion valuation

Heron Power ($140M, energy tech): The renewable grid hardware startup founded by former Tesla executive Drew Baglino closed a $140 million round backed by Andreessen Horowitz and Breakthrough Energy Ventures

Code Metal ($125M, AI coding): The Boston-based AI code translation startup raised $125 million in Series B funding led by Salesforce Ventures, just three months after its Series A

ECONOMIC SNAPSHOT

US economy slowed sharply in the fourth quarter, expanding at a rate of just 1.4% (CNN, 4 minute read)

The U.S. economy slowed sharply in late 2025, with Q4 GDP growing at 1.4%, down from 4.4% in Q3 and below expectations. For the full year, growth came in at 2.2%, the weakest since 2020. The government shutdown cut 1.1 percentage points from fourth-quarter growth, and consumer spending slowed to 1.4%, though wealthier households continued to support overall activity despite tariffs, immigration restrictions, and weak job creation. Business investment rose to 3.7%, helped significantly by AI-related spending

However, household finances showed strain: December consumer spending rose 0.4% (just 0.1% after inflation), incomes increased 0.3% but were flat in real terms, and the savings rate fell to 3.6%, its lowest since October 2022

Sentiment diverged sharply between higher- and lower-income households

Inflation picked up again, with the Fed’s preferred gauge, PCE inflation at 2.9% annually and core PCE at 3%, the highest in nearly a year

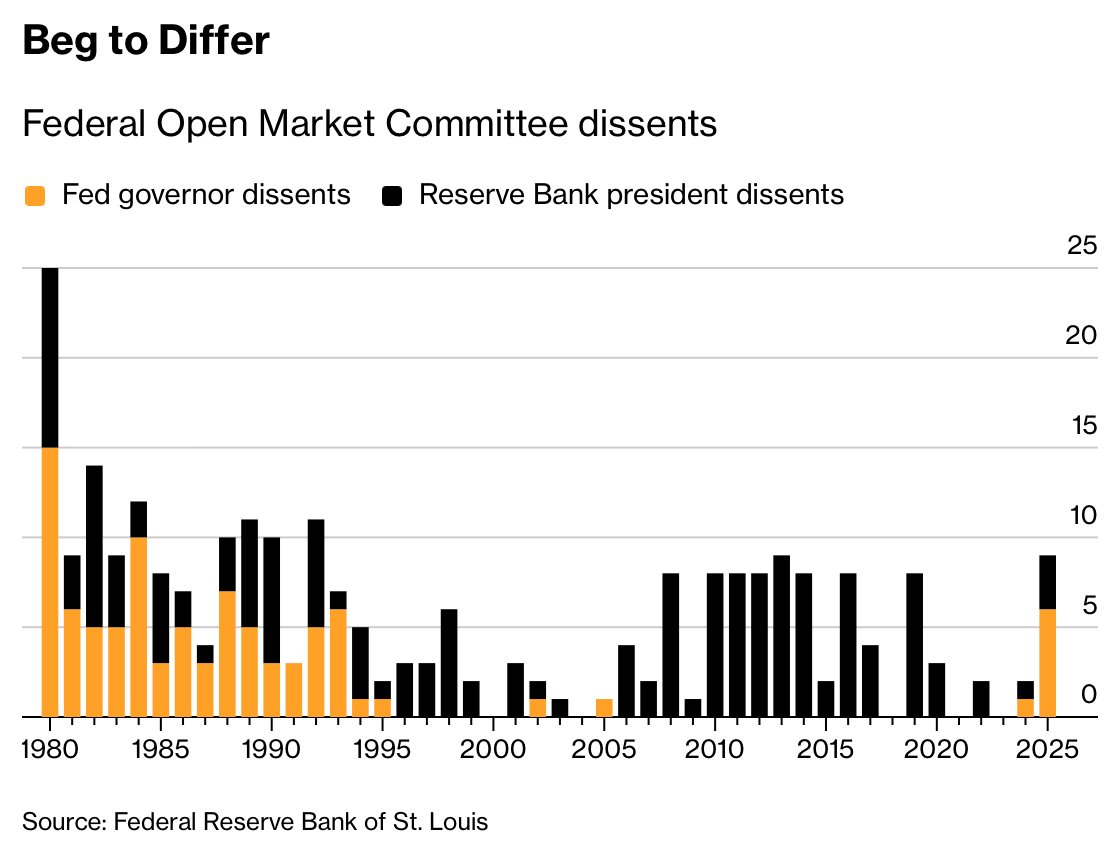

How Jerome Powell Is Trump-Proofing the Fed (Bloomberg, 6 minute read)

The Federal Reserve’s December meeting produced a rare 9–3 split vote, with Chair Jerome Powell backing a 0.25 percentage point rate cut, two officials opposing any cut, and one calling for a larger reduction. Dissents have surged recently, 10 in the past five meetings, versus 16 in Powell’s first 61, signaling growing internal debate as the benchmark rate stands at 3.5%–3.75%. The divide comes as President Trump pushes for rates as low as 1% and has nominated Kevin Warsh to replace Powell in May

January minutes show officials increasingly cautious about further cuts, while Trump allies have sought to reshape the Fed’s board, including a legal attempt to remove a governor

Powell has countered by reinforcing Fed independence, holding nearly 80 meetings with lawmakers in 2025, up about 60% year over year

He has also signaled he could remain on the board until 2028, preserving influence even after his chair term ends

Despite tariff teardown, the road ahead for private markets remains murky (PitchBook, 3 minute read)

President Trump vowed to press ahead with tariffs despite a 6–3 Supreme Court ruling striking down most of them, signaling he may use alternative legal tools, including Section 122 of the 1974 Trade Act, to impose a temporary 10% global tariff for up to 150 days. The decision leaves uncertainty for investors, particularly in private equity, where tariff fears had already pushed U.S. manufacturing deal volumes to decade lows. The ruling shifts responsibility to the U.S. Court of International Trade, raising questions about how companies might reclaim an estimated $170 billion in duties collected since last year

A wave of refund requests could create significant bureaucracy and short-term disruption

Markets reacted modestly, with the S&P 500 up 0.69%, but renewed tariff threats risk prolonging volatility

Tariff uncertainty has already delayed IPOs and complicated cross-border dealmaking, and further escalation could create new headwinds for public listings and private market exits

E.U. hits the brakes on U.S. trade deal after Trump threatens 15% global tariffs (NBC News, 4 minute read)

The European Parliament has halted ratification of its trade deal with the U.S. following the Supreme Court’s decision to strike down most of President Trump’s tariffs, citing uncertainty over whether Washington can uphold its commitments. Lawmakers said the U.S. position is now “uncertain,” especially after Trump threatened countries with “much higher” tariffs in response to the ruling

Markets reacted negatively: the Dow fell more than 710 points (-1.4%), the S&P 500 dropped 1%, the Nasdaq declined 1.3%, and Europe’s Stoxx 600 slipped 0.2%

The original deal, reached last July, capped most U.S. tariffs on EU goods at 15% and eliminated tariffs on select sectors like aircraft parts and semiconductors

Complicating matters, Trump signed a new executive order imposing a 10% global tariff, later saying it would rise to 15%, even as duties invalidated by the Court are set to stop being collected

Trump’s scramble to fix his crumbling tariff strategy sows global chaos and confusion (The Guardian, 4 minute read)

President Trump promoted a proposed $550 billion Japanese investment pledge as evidence that tariffs are working, but days later the Supreme Court struck down much of his tariff regime, creating fresh uncertainty. For now, most countries face a blanket 15% tariff on exports to the US under a temporary 150-day authority, disrupting trade deals and prompting the EU to pause ratification

While the administration argues tariffs help the US, New York Fed analysis estimates 90% of the cost falls on US companies and consumers, and the US trade deficit recently hit a record high

Meanwhile, exports from China (+6.1% overall), India (+2.2%), and Japan (+16.8% in January) have remained resilient, complicating claims that the US is clearly winning the trade fight

Ahead of State of the Union, what is the state of the US economy? (USA Today, 4 minute read)

Ahead of President Trump’s Feb. 24 State of the Union, the economic picture is mixed. Inflation has cooled more than expected, job growth accelerated in January, and larger tax refunds this spring could provide a near-term boost. Still, growth has been narrow: January job gains were concentrated in health care and social assistance, AI-related investment is driving much of GDP, and consumer confidence has fallen to its lowest level since 2014. Economists describe 2025 growth as “adequate” but uneven, with risks tilted toward a weaker labor market in 2026

While tariffs and policy shifts have added volatility, analysts see limited immediate macro impact from the recent Supreme Court ruling, especially after Trump announced a new 15% global tariff

Many warn the economy looks “K-shaped,” with wealthier households and AI-driven sectors doing well while lower-income Americans continue to struggle with high prices and rising debt

The result is an economy that looks stable in headline data but feels far less secure for many households

IPOs & EXITS

US VC Secondary Market Watch (PitchBook, 15 minute read)

2026 is set to be a turning point for the U.S. venture secondary market, which reached an estimated $106.3 billion in 2025, nearing IPO and M&A scale. Direct secondaries totaled about $91.7 billion (midpoint estimate), but activity remains highly concentrated, with the top 20 startups accounting for 86.4% of Q4 trading value. Upcoming mega-IPOs could cause short-term volume dips but improve long-term price discovery. Secondaries are increasingly viewed as structural, not cyclical

Dedicated dry powder hit $11.8 billion (up 2.8x since 2022), though still just 3.9% of primary VC capital, signaling room for growth

AI, crypto, defense, and aerospace dominate activity, with AI capturing 65.4% of primary VC deal value in 2025

Tender offers are becoming standard liquidity tools, including OpenAI’s $6.6B and SpaceX’s $2.6B programs, while SPVs face tighter regulatory scrutiny

Banks Pounce on M&A Comeback With $100 Billion of Buyout Debt (Bloomberg, 4 minute read)

Debt bankers are riding a sharp rebound in M&A, with roughly $100 billion in leveraged buyout debt in the pipeline, most underwritten in recent months. Including investment-grade deals, total acquisition financing exceeds $100 billion, putting 2026 on pace to rival 2021’s record year. Major transactions include €4 billion for Carlyle’s BASF deal, $3.75 billion for BP’s Castrol unit, and a $20 billion financing for the record Electronic Arts buyout

After a slowdown since 2022, private equity exits and corporate carve-outs are driving activity, with some deals rumored at up to $25 billion

Strong demand for risky debt, such as the $8.75 billion syndicated portion of Hologic’s $18 billion acquisition, suggests credit markets can absorb the surge, even as banks move quickly to offload risk

Robinhood’s $1 Billion Fund Pitches Pre-IPO Stock as Next Craze (Bloomberg, 3 minute read)

Robinhood is seeking to raise $1 billion through the IPO of a closed-end fund, offering 40 million shares at $25 each (5 million from Robinhood and 35 million from the fund). Trading is expected to begin Feb. 26. The fund aims to give retail investors access to private companies such as Databricks, Oura, Revolut and Stripe, capitalizing on renewed interest in pre-IPO names like SpaceX, which could raise up to $50 billion in a future listing

The vehicle will invest in at least 10 private companies, with no single holding exceeding 20% of assets

It will charge a 2% management fee (reduced to 1% for the first six months) and no performance fee

Closed-end funds can trade at premiums or discounts to net asset value, a structure that has historically limited demand, only 46 new CEFs have launched since 2019, and the first such IPO this year raised just $53 million

WHAT A TIME TO BE ALIVE

VCs are pushing back against California’s new startup diversity reporting rules (PitchBook, 3 minute read)

California’s Fair Investment Practices by Venture Capital Companies Act, passed in October 2023 and amended in 2024, requires VC firms with a nexus to California to disclose demographic data on founders tied to their 2025 investments. Firms had to register by March 1, with detailed reporting due by April 1. Founders can voluntarily disclose information including race, gender, sexual orientation, disability status, veteran status, and California residency

Industry groups, including the NVCA, argue the rollout has been rushed, noting that the required survey form was released only one month before reporting deadlines

They also warn the law’s scope is broad and unclear, potentially applying to all 2025 investments made by firms connected to California, and that voluntary participation could lead to incomplete or misleading data

Firms that fail to comply face penalties of up to $5,000 per day after a 60-day notice period, creating legal and operational risk for investors navigating the new reporting regime

AI8 VENTURES HIGHLIGHT

State of VC Report: The AI Power Law

“Every technological revolution has two halves: the bubble and the golden age that follows.”

The stock market is at all-time highs, but inflation remains sticky and the job market is weakening. Ask around and you’ll hear the same refrain: the labor market feels tougher than ever. At the same time, the first wave of AI agents is “joining the workforce”. Imagine a software engineering agent capable of performing most tasks of a mid-level developer. Now imagine thousands. Extend that across every knowledge field, and the implications for productivity, and potential displacement, are profound.

What happens when the next round of layoffs hits? Add tariffs on top, and ask what happens if consumption weakens. Even the Federal Reserve admits it is unsure of what comes next.

Against this backdrop, venture capital in 2025 is not in recovery but in recalibration. The illusion of recovery is powered almost entirely by AI. Capital is flowing, but to fewer companies than ever. Outside AI, down rounds are rising, and nearly half the unicorn population hasn’t raised since 2022.

We are living in an AI bubble. Just four mega caps, Nvidia, Meta, Microsoft, and Broadcom, accounted for 60% of the S&P 500’s gains, with Nvidia alone responsible for more than a quarter. It’s a paradox. Yes, we’re in a bubble, but it’s also the future. We are witnessing what may be the most important technological shift in a generation. It’s hype layered on top of something undeniably real.

Uncertainty is the name of the game; not one single path forward, but divergent scenarios. Alpha will be earned through selectivity, by navigating volatility rather than avoiding it.

8alpha.ai is an AI fintech transforming cash-generating businesses into scalable, AI-powered companies. We provide revenue-based financing and hands-on AI transformation, delivering no zeros with unlimited upside. We’re the architects building financial infrastructure for the next generation of investors and startups.

Become part of our revolution.

Happy reading,

8alpha.ai’s Research & Investment Team