- AlphaInsights by 8alpha.ai

- Posts

- Oil, AI, and the New World Economy

Oil, AI, and the New World Economy

Nicole Rojas

April 13, 2026

Week of April 13th, 2026

Welcome to AlphaInsights, 8alpha.ai’s weekly newsletter, your ultimate source for curated insights and key updates from the dynamic world of venture capital!

From billion-dollar rounds to market-defining shifts, we deliver the intelligence powering the global investment landscape, moving investors and innovators forward. At 8alpha.ai, we’re not waiting for the future of capital, we’re building it. Stay sharp, stay curious, and stay ahead.

STARTUPS

ROUNDS AND UNICORNS

The Week’s 10 Biggest Funding Rounds: SiFive Leads With $400M For Custom Chip Designs As Aviation, Biotech And Defense Startups Also Raise Big (Crunchbase, 5 minute read)

SiFive (Semiconductors): Raised $400M Series G, positioning itself for a potential IPO. The company provides chip design blueprints used by firms like Alphabet, benefiting from growing demand for custom AI chips and alternatives to traditional architectures

Hermeus (Autonomous Defense): Raised $200M equity + $150M debt, reaching a $1B valuation. The company is developing high-speed autonomous military aircraft, reflecting increased defense spending and geopolitical demand

Sidewinder Therapeutics (Biotech): Raised $137M Series B to advance its pipeline of antibody-drug conjugates (ADCs) into clinical trials, targeting hard-to-treat cancers with precision therapies

Aria Networks (AI Infrastructure): Raised $125M Series A to build AI-driven networking platforms that optimize data center performance, supporting the rapid scaling of AI workloads

Starfish Space (Aerospace): Raised $111.7M Series B to develop autonomous spacecraft for satellite servicing and debris removal

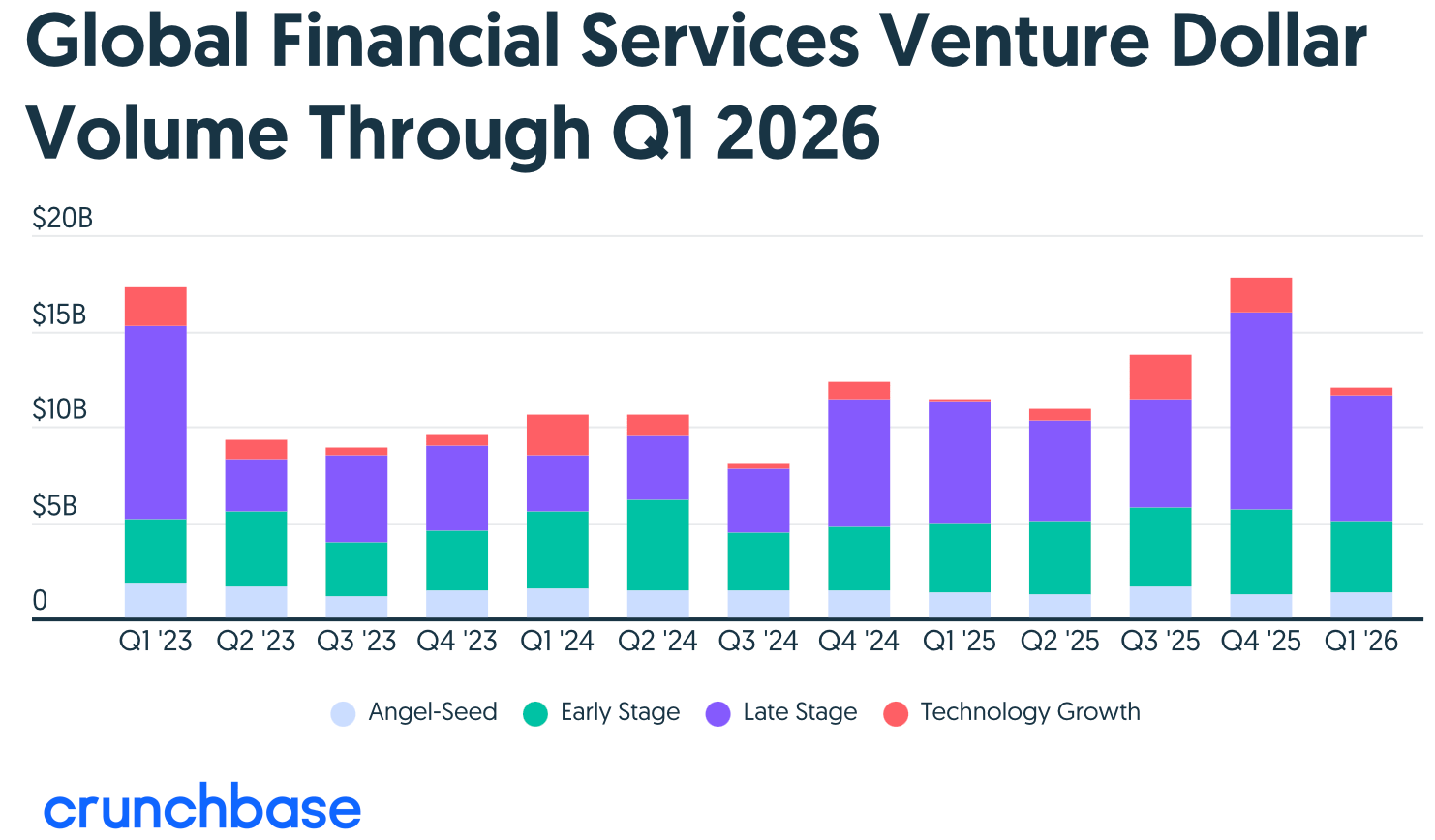

Fintech Startups Globally Raise More Money In Far Fewer Deals In Q1 2026 (Crunchbase, 4 minute read)

Fintech funding is rising but becoming more concentrated, with $12B invested across 751 deals in 2026 (+5% YoY, but -31.5% deal count), signaling larger round sizes. Growth has been driven by late-stage funding ($6.9B, +8% YoY), though activity has slowed sequentially, down 33% from $17.8B in Q4 2025. Despite macro uncertainty and a 33% QoQ funding slowdown, investors remain bullish, particularly on AI-driven fintech and stablecoin infrastructure, with strong focus on enterprise applications and automation

The U.S. dominates, capturing $6.3B (~50% of global funding, +47% YoY), while large rounds continue to drive valuations

IPO activity will depend on market conditions and the performance of mega listings like SpaceX, OpenAI, and Anthropic

ECONOMIC SNAPSHOT

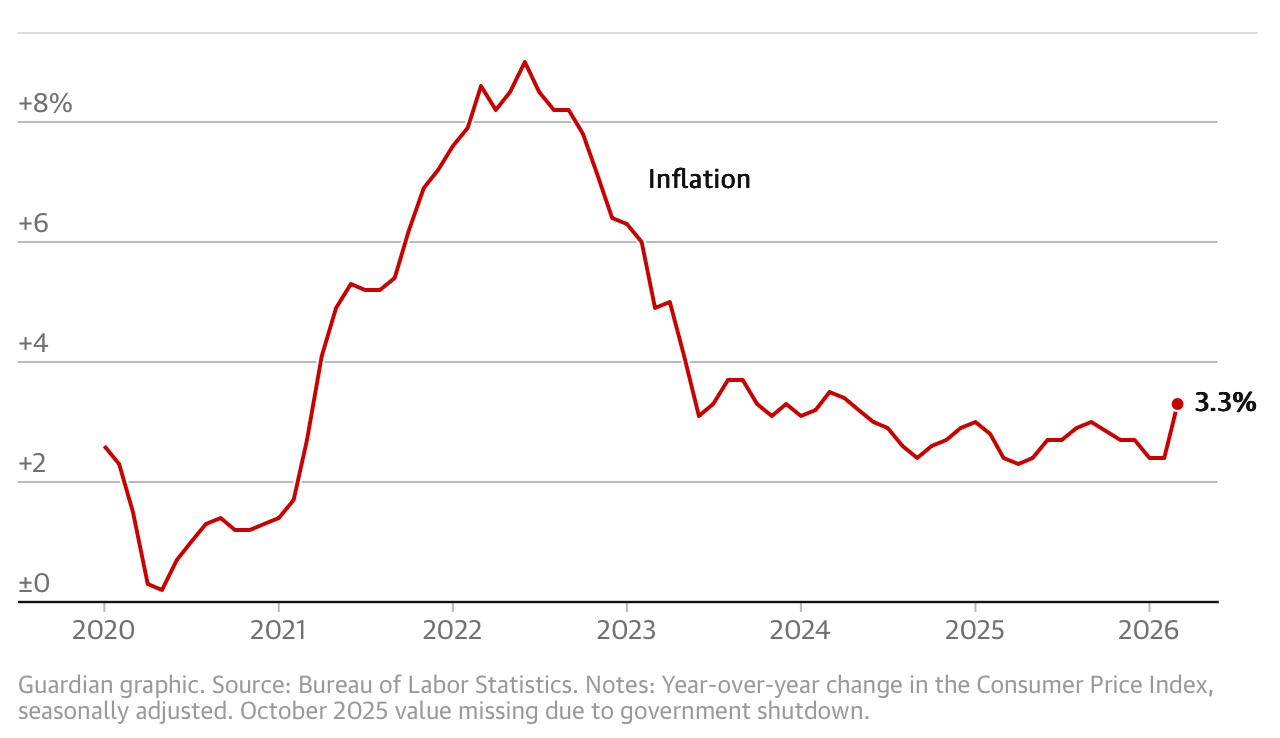

US inflation soars in March as war on Iran drives economy into uncertainty (The Guardian, 4 minute read)

U.S. inflation surged in March, with CPI rising 0.9% MoM and 3.3% YoY, marking the largest monthly increase in nearly two years, driven by the Iran conflict and energy shock. Energy prices jumped 10.9%, including a 21.2% spike in gasoline, while oil remained elevated (~+10% vs. pre-conflict, +30% YTD) due to disruptions in the Strait of Hormuz, which handles ~20% of global energy flows

Core inflation remained moderate (0.2% MoM, 2.6% YoY). However, broader economic signals weakened, with GDP revised down to 0.5%, producer prices rising sharply, and consumer confidence dropping 10.7% to a record low

The labor market remained resilient (178K jobs, 4.3% unemployment), complicating the Fed’s response to rising inflation

Consumer Spending, Engine of the U.S. Economy, Is Under Strain (The New York Times, 4 minute read)

Rising energy prices from the Iran conflict are starting to squeeze U.S. consumers, lifting everyday costs, from groceries to transportation and forcing households to cut discretionary spending. While consumer spending (~⅔ of U.S. GDP) has remained resilient, supported by strong asset prices (equities up ~24% YoY and home values up 50%+ over five years) and tax refunds, underlying pressures are building as wage growth slows, savings rates fall to near-2008 lows, and gas spending rises (+20% YoY)

Higher energy costs act like a tax on consumers, while weaker “wealth effects” from markets further reduce spending

Economists warn that sustained shocks, such as oil above $120/barrel or a ~20% market drop, could trigger a sharper pullback in consumption and potentially a recession

Nonetheless, growth is still projected at ~2.3% in 2026

Trump’s strait blockade risks another serious blow to the global economy (CNN, 7 minute read)

Failed U.S.-Iran talks have pushed the Trump administration toward a risky strategy, including a proposed blockade of the Strait of Hormuz, aimed at cutting Iran’s oil revenues but with major global economic consequences. The announcement already triggered market reactions, with oil prices jumping 8% to ~$104/barrel and U.S. gasoline prices exceeding $4/gallon, contributing to inflation rising to 3.3% in March

While the blockade could further weaken Iran’s economy, it risks disrupting global energy flows through the Strait of Hormuz, which carries ~20 million barrels/day (~20% of global oil supply)

This could push oil prices higher, strain relations with major economies like China, and impact U.S. allies heavily reliant on Gulf energy

The Iran War Has Finally Shattered America’s World (Bloomberg, 7 minute read)

The Iran conflict is accelerating a shift toward a more fragmented and “weaponized” global economy, where critical dependencies, especially energy, are used as leverage, with the Strait of Hormuz highlighting systemic vulnerability. Rising energy prices (oil +30% YTD in recent data), supply chain risks, and geopolitical fragmentation are increasing costs and uncertainty across markets, while pushing countries to invest in resilience (e.g., alternative supply routes, domestic production)

At the same time, the war is reinforcing structural shifts, including rising defense spending (NATO members targeting ~2–5% of GDP), intensified great-power competition, and increased capital allocation toward strategic sectors like AI, infrastructure, and energy security

As a result, markets are becoming more volatile, with growth and investment increasingly shaped by geopolitical risk

IPOs & EXITS

Anthropic may have closed the revenue gap on OpenAI. Here's what it means for their IPOs (Reuters, 4 minute read)

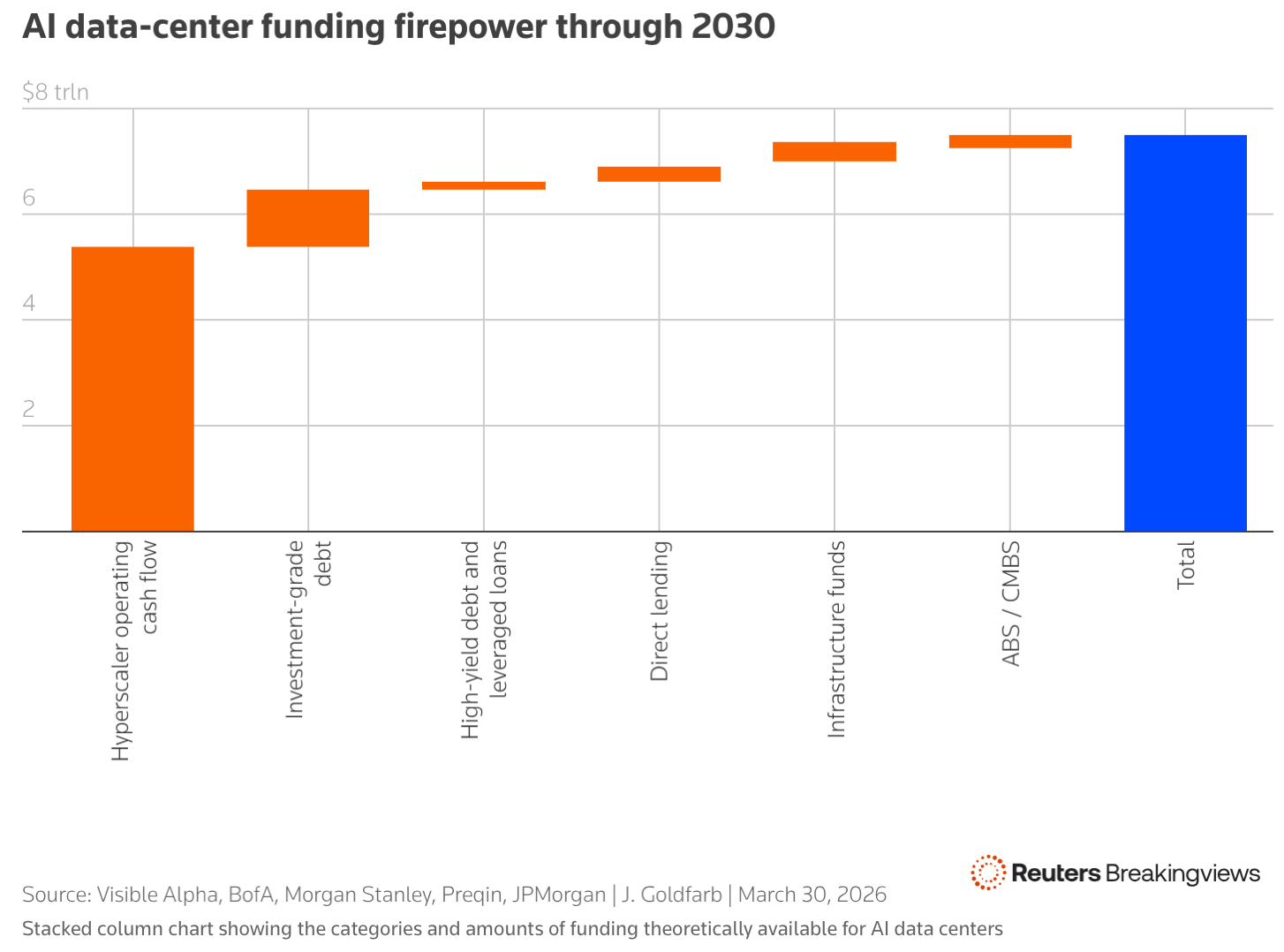

A wave of mega IPOs, led by SpaceX (potentially June 2026), followed by OpenAI and Anthropic later in the year, is expected to absorb a significant share of investor demand, potentially crowding out other large tech listings and delaying a broader IPO market reopening until 2027. At the same time, competition between OpenAI and Anthropic is intensifying, with Anthropic reaching ~$30B annualized revenue vs. OpenAI’s ~$24B, driven by enterprise adoption and high-value AI workloads rather than user scale

However, the broader AI expansion faces structural limits, as projected data center buildouts could require $6.6T–$8.8T by 2030, roughly in line with total available funding

Anthropic’s product momentum has already had material effects on public markets, contributing to a ~$1T sell-off in software stocks earlier in the year

Why Starlink is so important to SpaceX's IPO (Yahoo Finance, 6 minute read)

SpaceX’s potential IPO, valued at up to ~$2T, is largely a bet on Starlink, which has evolved from an engineering project into the company’s dominant revenue and profit engine. Starlink generated ~$10.6B in revenue (≈67% of total) and ~$5.8B EBITDA (~54% margins), with 9M+ subscribers across 155+ countries, supported by a massive 9,600+ satellite constellation that continues to expand at industrial scale

Its vertically integrated model creates a strong cost advantage and high-margin recurring revenue, more akin to a software business than traditional telecom

Growth is further driven by new segments like direct-to-cell (6M+ users), enterprise, aviation, and government services, significantly expanding its addressable market

The IPO is essentially a bet on Starlink, positioning SpaceX as a high-growth global connectivity platform

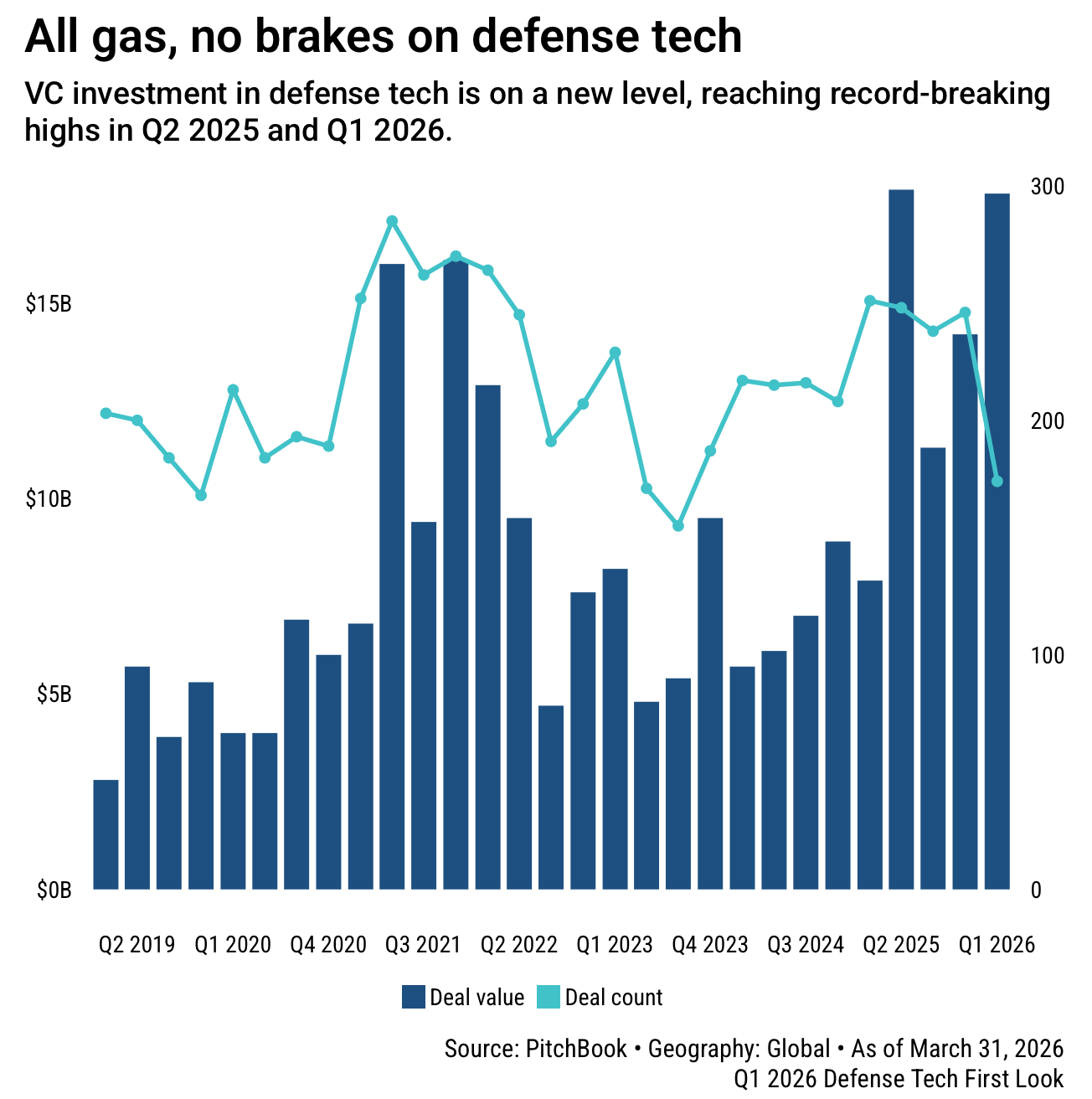

SpaceX isn’t the only defense tech IPO that VCs should care about (PitchBook, 4 minute read)

HawkEye 360, a satellite-based defense tech company, is preparing to go public as a smaller test case ahead of mega listings like SpaceX, offering an early signal for investor appetite in the sector. The company showed strong traction, with revenue rising 75% to $117.7M in 2025, backlog surging 6x to $302M, and both net income and EBITDA turning positive, reflecting growing demand for its signals intelligence platform

The business is driven by rising global defense spending and geopolitical tensions, with 61% of revenue from U.S. government contracts and ~$46M (~25%) from international customers

Its performance post-IPO will be closely watched, as it represents a typical VC-backed defense tech model: high growth, heavy investment, and increasing relevance as governments expand spending on surveillance and security infrastructure

WHAT A TIME TO BE ALIVE

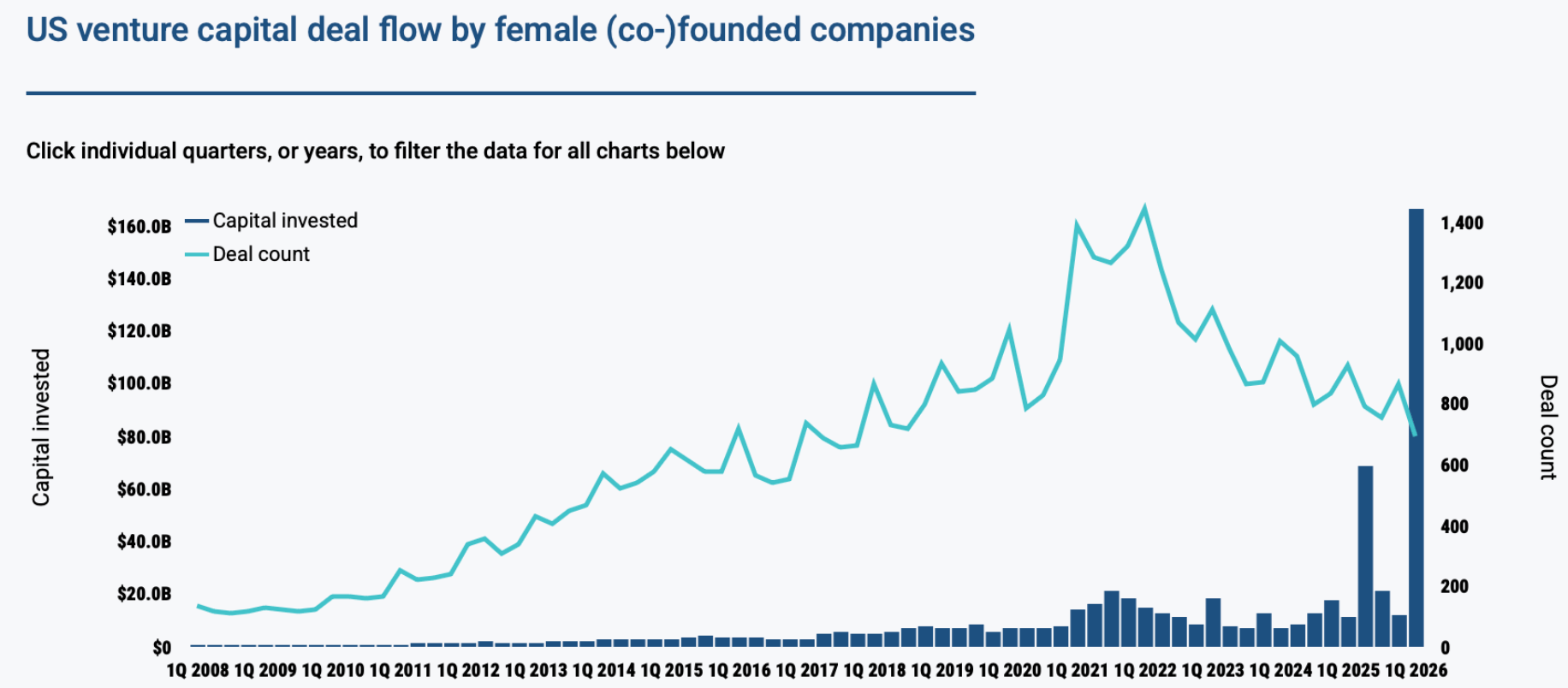

US VC female founders dashboard (PitchBook, 5 minute read)

Venture capital funding for female-founded startups in the U.S. has stabilized after a steep decline from the 2021 peak. While women-led companies now represent a smaller share of total VC deals, they continue to capture a growing portion of total capital raised, signaling stronger deal quality and investor confidence. In Q1 2026, women co-led companies raised $166.1 billion across 690 deals (vs. $51 billion across 880 deals in Q1 2025)

Female-only founded companies captured 6.2% of total deal count, while female-and-male co-led teams account for 17.7%

In terms of capital, female-only teams received 0.6% of total VC investment, compared to 62.6% going to mixed-gender founding teams

According to PitchBook data, the trend shows steady progress across states, industries, and stages, highlighting a sustained shift toward greater inclusion and visibility for women founders in the U.S. venture ecosystem

8ALPHA.AI HIGHLIGHT

“The winners will be those who own and integrate AI as a core means of production.”

With billion-dollar headlines, capital concentration, mega deals, and trillion-dollar AI valuations, something is clear: traditional VC is structurally broken and misaligned with current market dynamics. The question isn’t whether we’re in a bubble. We are. And the clock is ticking.

The real question is: when it bursts, and how you’re positioned when it does.

Everyone is asking how to build the next AI giant and ride the hype.

Fewer are asking: where is the real return in AI?

In this interview with the New America Alliance (NAA), a nonprofit dedicated to empowering Latino talent through access to capital, our CEO, Carlos Ochoa, breaks it down:

There are two paths:

The engineering moonshot: a capital-intensive, winner-takes-most race to build the next foundational model

The strategy: applying AI to transform cash-generating companies into scalable, high-efficiency growth engines

At 8alpha.ai, we’re focused on the second.

We use AI-powered financial operations and revenue-share financing to help companies become more efficient, scalable, and investor-ready.

Because in the AI era, profitability won’t just come from using the tools. It will come from owning the infrastructure and shaping the new means of production.

Key highlights:

“Started my first company at 19—it left me homeless. Best lesson ever.”

Carlos Ochoa co-founded one of Latin America’s largest cybersecurity firms and built an AI-driven fintech acquired by a European bank—each chapter reinforcing one conviction: AI is not a feature. It’s infrastructure

Carlos is now running Alpha Impact 8 Ventures and 8alpha.ai in San Francisco

Watch the full interview to rethink your AI strategy, avoid inflated valuations, and understand our thesis: “no zeros, unlimited upside.”

State of VC Report: The AI Power Law

“Every technological revolution has two halves: the bubble and the golden age that follows.”

The stock market is at all-time highs, but inflation remains sticky and the job market is weakening. Ask around and you’ll hear the same refrain: the labor market feels tougher than ever. At the same time, the first wave of AI agents is “joining the workforce”. Imagine a software engineering agent capable of performing most tasks of a mid-level developer. Now imagine thousands. Extend that across every knowledge field, and the implications for productivity, and potential displacement, are profound.

What happens when the next round of layoffs hits? Add tariffs on top, and ask what happens if consumption weakens. Even the Federal Reserve admits it is unsure of what comes next.

Against this backdrop, venture capital in 2025 is not in recovery but in recalibration. The illusion of recovery is powered almost entirely by AI. Capital is flowing, but to fewer companies than ever. Outside AI, down rounds are rising, and nearly half the unicorn population hasn’t raised since 2022.

We are living in an AI bubble. Just four mega caps, Nvidia, Meta, Microsoft, and Broadcom, accounted for 60% of the S&P 500’s gains, with Nvidia alone responsible for more than a quarter. It’s a paradox. Yes, we’re in a bubble, but it’s also the future. We are witnessing what may be the most important technological shift in a generation. It’s hype layered on top of something undeniably real.

Uncertainty is the name of the game; not one single path forward, but divergent scenarios. Alpha will be earned through selectivity, by navigating volatility rather than avoiding it.

8alpha.ai is an AI fintech transforming cash-generating businesses into scalable, AI-powered companies. We provide revenue-based financing and hands-on AI transformation, delivering no zeros with unlimited upside. We’re the architects building financial infrastructure for the next generation of investors and startups.

Become part of our revolution.

Happy reading,

8alpha.ai’s Research & Investment Team